TVJ Stories

MiniLED & OLED Display: The battle for the IT market

MiniLED-based displays have been introduced by top consumer brands such as Samsung, LGE, TCL, Apple and others for TV, monitor, notebooks and tablets.

By the use of multi zone blinking backlights, miniLED with quantum dots (QDs) can enable LCDs to have higher brightness, very high contrast, excellent HDR, thin form-factor, superior power efficiency and display performance close to OLED. OLED display technology has secured a strong position in the premium TV market and is increasing its share in the smartphone market. (although that growth is slowing – editor OLED Adoption by Smartphones to Slow Down in 2022)

The IT market has been dominated up to now by LCD technology (based on a-Si, LTPS and Oxide substrates). However, OLED display demand is starting to increase for IT applications, which is leading suppliers to invest in 8.5 RGB OLED fabs to expand capacity and reduce cost. The MiniLED vs OLED display battle will intensify in the next few years with technology developments, cost improvements, higher production and increased adoption rates. The battle can actually help the display industry with new opportunities for differentiated products and better replacement demand.

MiniLED: Empowers LCD

By the use of multi zone blinking backlights (>10,000 zones), miniLED can enable LCD to have higher brightness (>1000 cd/m²), very high contrast (>1,000,000:1), excellent HDR, better color rendering, ultra thin form factor, superior power efficiency and display performance close to OLED. Due to miniLED’s small size, it can enable curved form factors and narrow bezels. MiniLEDs can use existing fabs without major investments. Major LED chip companies such as Ennostar (Epistar + Lextar) (Taiwan) and San’an (China) have been increasing their capital expenditure and capacity. More collaboration is happening among suppliers within the miniLED supply chain: that means the substrate, LED epitaxial wafer, LED packaging, driver ICs, display suppliers and even the consumer electronic companies. Panel suppliers are collaborating with their LED subsidiaries.

The year 2021 has been a pivotal year for miniLED with more product introductions for multiple applications. Top consumer brands Samsung and LG Electronics joined TCL in introducing miniLED-based LCD TV products combined with QDs at CES 2021. The growth in the use of miniLED backlights combined with QDs lead to higher picture quality enabling further growth driving an expansion phase in 2021 and 2022.

Apple’s introduction of miniLED-based products for the iPad Pro and MacBook Pro has really helped its growth in the IT market. More suppliers are expected to enter in 2022, increasing competition, improving the supply chain, increasing volumes, improving yield and reducing cost. MiniLED-based products with higher picture quality, more competitive prices, higher product availability and brands focus (for product differentiation) will drive shipment growth in 2022.

MiniLED : Cost still a challenge for IT market

MiniLED costs have gone down recently due to increased efficiency and lower chip costs. However, it still faces cost challenges to become competitive. Cost reduction can be realized through advanced chip production and higher throughput for the transfer and assembly process and PCB and driver IC enhancements. Chip production can be improved through reductions in chip size, improvements in uniformity and boosting luminous efficiency. Panel suppliers and component suppliers are expected to focus more on cost reductions in 2022 to support brands’ product introduction of miniLED-based displays to drive growth and expansion plans.

OLED: Increasing focus for IT market

The high cost of OLED displays can also be a limitation for the IT market. Demand for OLED displays for tablets, notebooks and monitors is increasing. OLED display suppliers are planning to develop 8.5Gen RGB OLED fabs. According to an article by Ross Young of DSCC, published on Feb 14, 2022 (registration required),

- There are now 11 different 15K G8.5/G8.6 IT OLED lines under development.

- IT fab spending is expected to increase every year from 2021 to 2025.

- Both BOE and Visionox have switched their next smartphone fabs to these cost optimized IT RGB OLED fabs, and hope to narrow the cost gap with LCDs in notebooks and other applications.

- SDC and LGD are also expected to build these lines.

- The cost reduction opportunities lie with changing the backplane from LTPS or LTPO to IGZO (which has many fewer masks).

- There are additional cost savings expected by switching from a flexible substrate to a rigid + TFE substrate which should reduce the capex and process steps from the PI coating, PI curing, additional CVD barrier layer and laser lift-off (LLO) steps and also boost yields.

- There are additional productivity/depreciation expense gains from using G8.5 equipment rather than G6 equipment as although the glass size is around 2X larger, the equipment cost is usually much less.

- These new fabs will bring some significant changes to OLED manufacturing. First, we will likely see a full G8.5 vertical FMM VTE system in the market as opposed to existing ½ G6 horizontal systems.

According to the article, notebooks are likely to be initial target of these 8.5 OLED fabs. However some obstacles for OLED penetration for notebooks include: single dominant supplier (SDC), higher power consumption than LCD, lack of rigid + TFE capacity, lack of IGZO backplanes and a lack of tandem OLED lines to boost brightness, efficiency and lifetimes. The article also says “OLED power consumption could come down significantly though through the use of an auxiliary electrode, color on encapsulation, variable refresh with IGZO, a more efficient blue emitter, etc”.

According to DSCC, tablets are another natural opportunity for these fabs, which should be able to bring down costs vs. flexible G6 OLED lines. Up to now SDC and EDO have been the two OLED suppliers focusing on the tablet market. Monitors are another possibility for these fabs. OLEDs are better suited for high end monitors or gaming monitors which demand high refresh rates and are less cost sensitive. Technology development, improvements in materials, advancements in inkjet printing combined with capacity expansion and higher competition will help OLED display to gain a higher market share in the future.

QD-OLED: Entering the monitor market

At CES 2022, Samsung Display’s QD-Display (QD-OLED) became the world’s first display to integrate printed QDs with blue self-emitting pixels based on OLEDs. The company has introduced QD-Display for two TV sizes, 55” and 65”, along with a 34” curved gaming monitor panel. It has red and green QD material printed on each pixel that is not blue. QD-Display can provide superior color performance, as it does not rely on color filters like WOLED or LCD.

Both Samsung Electronics and Dell Alienware have announced new gaming monitors using the 34″ curved QD-OLED display. With higher display performance QD-Display (QD-OLED) curved gaming monitor expects to provide more immersive experience. Dell Alienware QD-OLED gaming monitor is now shipping for $1299.

MiniLED vs. OLED: Battle for IT market

In March 2022 DSCC published a series of articles with results from its “Quarterly Advanced IT Display Shipments and Technology Report (shows OLED vs. MiniLED LCD tablet, notebook, monitor and all in one (AIO)).

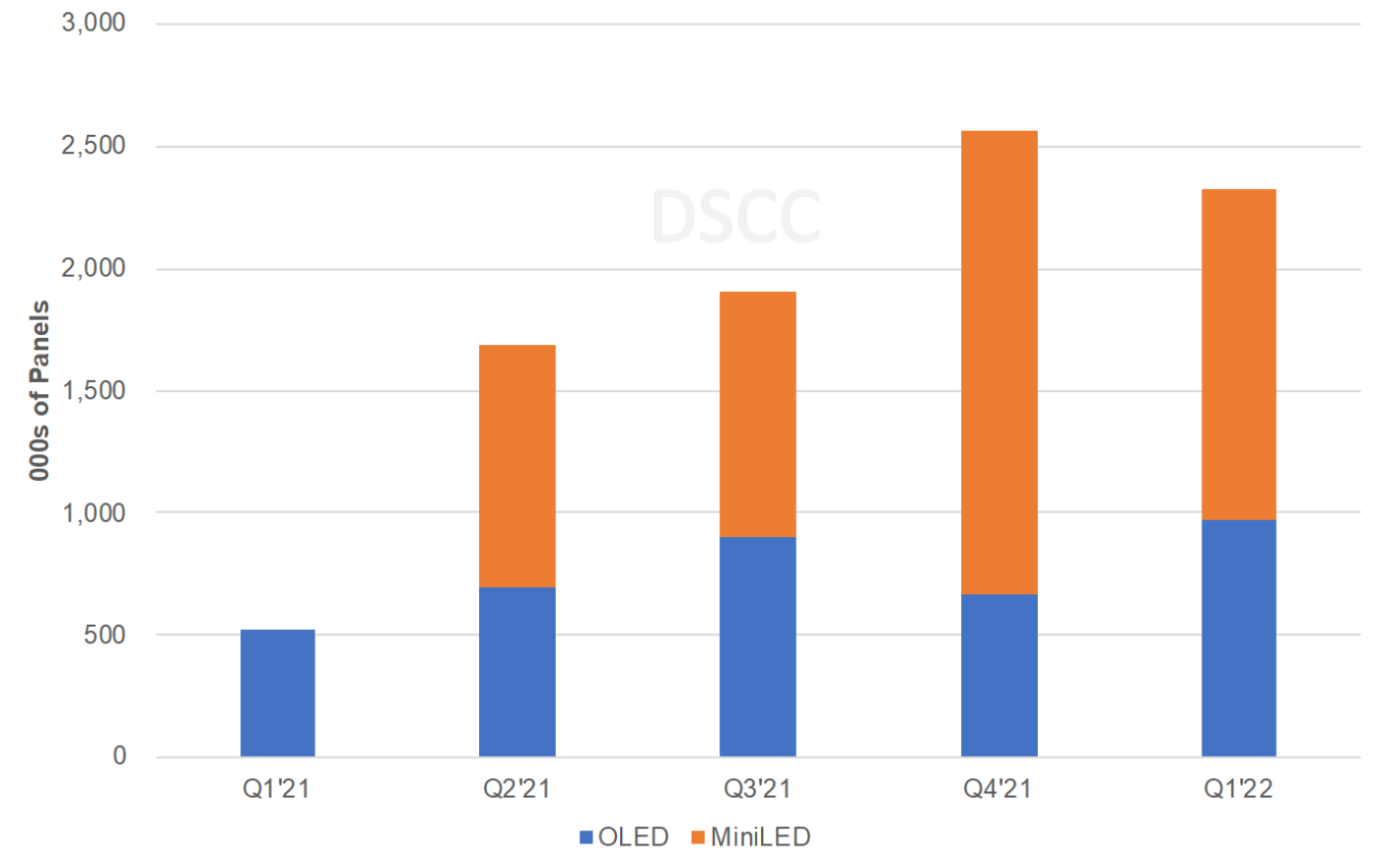

According to the DSCC article by Ross Young, in the advanced tablet market:

- Significant strides are being made by the Apple 12.9” iPad Pro.

- Despite MiniLED supply constraints, that product is dominating the Advanced Tablet market.

- Panel shipments to Apple for that product rose 90% Q/Q to 1.9 million units, enabling the entire segment to rise 35% Q/Q and 153% Y/Y to 2.57 million units, a quarterly record.

- MiniLEDs and Apple accounted for 74% of the Advanced Tablet Market in Q4’21 with just a single product.

- For all of 2021, the Advanced Tablet market rose 99% to 6.7 million units with MiniLEDs and Apple accounting for a 58% share and 2.8 million panels.

Advanced Tablet Display Shipments by Technology. Source DSCC

Advanced Tablet Display Shipments by Technology. Source DSCC

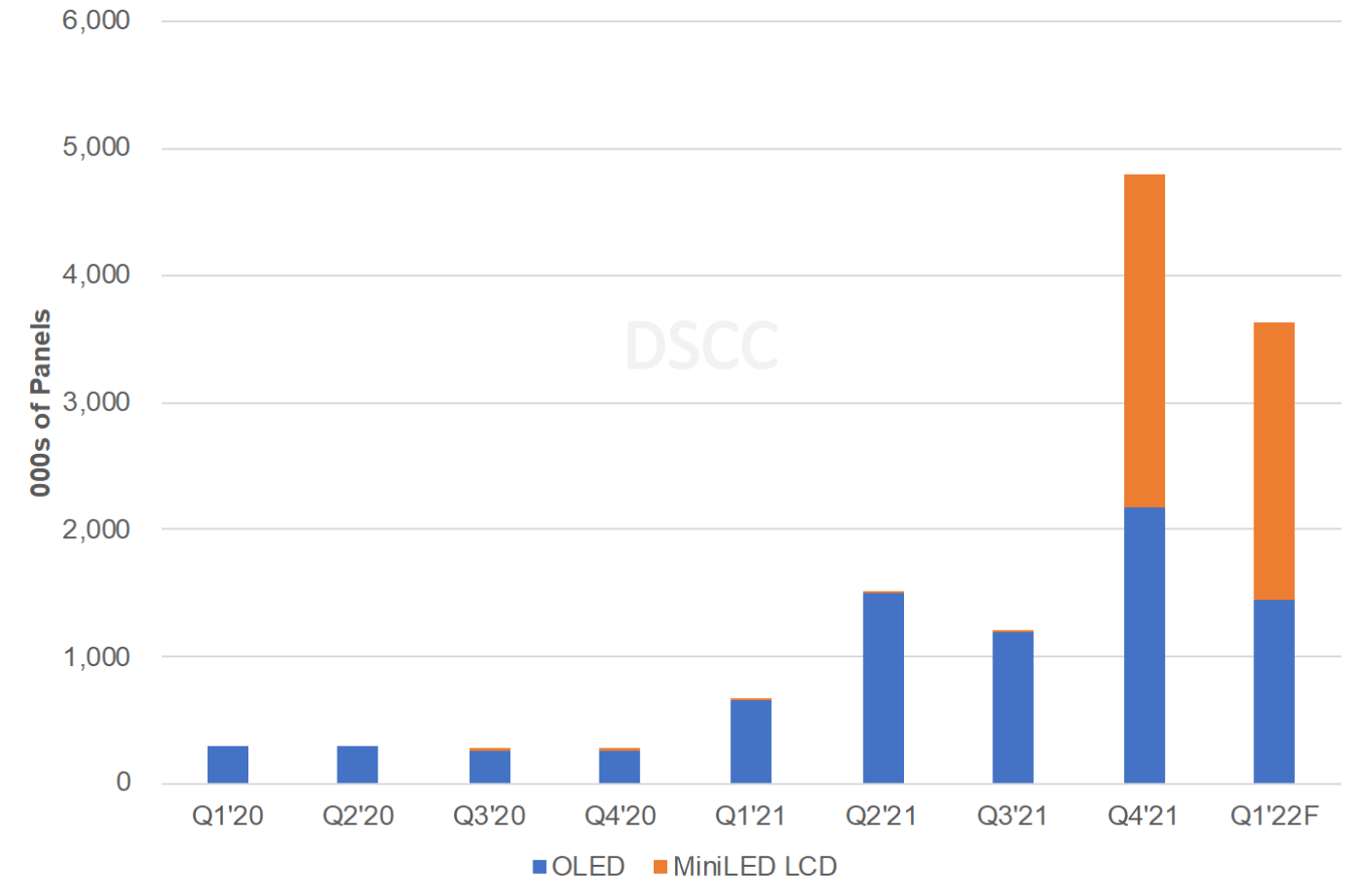

Another DSCC article focused on advanced notebook displays and shows:

- Q4’21 was a record quarter for Advanced Notebook displays rising 298% Q/Q and 1717% Y/Y to 4.8 million panels.

- On an annual basis, 2021 was up 629% Y/Y to 8.2 million panels. 2021 was 10% higher than predicted as both Apple’s MiniLED MacBook Pros and OLEDs outperformed in Q4’21.

- MiniLEDs surged to a 54% share in Q4’21 and earned a 32% share for the year on Apple’s successful launch of its 14.2” and 16.2” MacBook Pros.

Advanced Tablet Display Shipments by Technology. Source:DSCC

Advanced Tablet Display Shipments by Technology. Source:DSCC

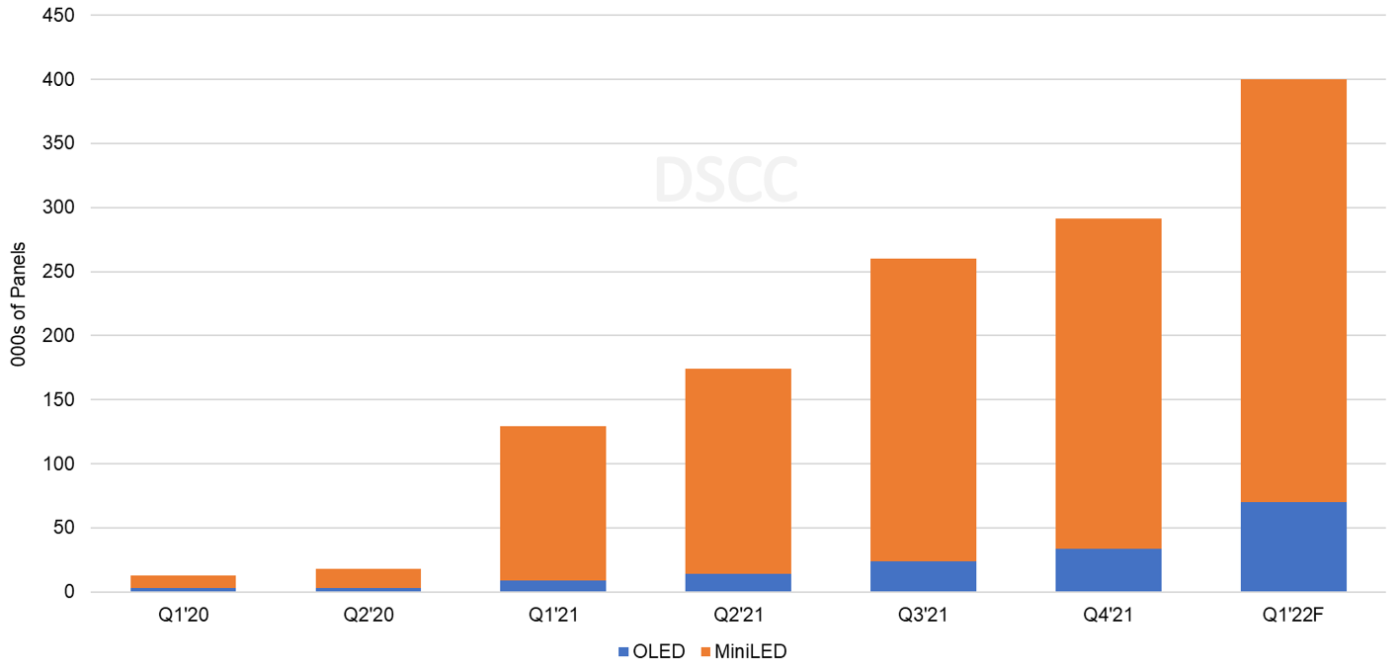

According to a DSCC article by David Naranjo covering advanced monitors:

- In 2021, the Advanced Monitor market rose 397% Y/Y as a result of increased panel procurement for the Asus 32” MiniLED models, the Apple 32” MiniLED model and LG’s 27” and 32” inkjet printed (IJP) RGB OLED models.

- In 2021, panel procurement of MiniLED monitors accounted for a 91% share in 2021. In 2022, with the launch of 42” and 48” WOLED models and more 27” and 32” IJP RGB OLED models, the MiniLED share is expected to decrease to 80%.

- In 2022, DSCC expects panel procurement for OLED monitor models to increase 612% Y/Y on the strength of new QD-OLED models and 42” and 48” WOLED models that were announced at CES 2022. Those models include the 34” QD-OLED models from Dell and Samsung, the 27” and 32” IJP RGB models from LG and the 42” and 48” WOLED models from LG and Asus.

- In Q2’22, Apple announced a 27” MiniLED monitor that is expected to drive significant panel procurement in 2022.

Advanced Monitor Display Shipments by Technology. Source:DSCC

Advanced Monitor Display Shipments by Technology. Source:DSCC

Apple is also expected to adopt OLED technology for its IT products in future years triggering more competition. MiniLED and OLED’s battle for the IT market can open up new opportunities for the display industry with product differentiation and will drive replacement demand with higher specs. Success will depend on each technology’s ability to reduce cost to drive demand. (SD)

The article, authored by Sweta Dash, President, Dash-Insights.

Was first published in Display Daily

You must be logged in to post a comment Login